All Categories

Featured

Table of Contents

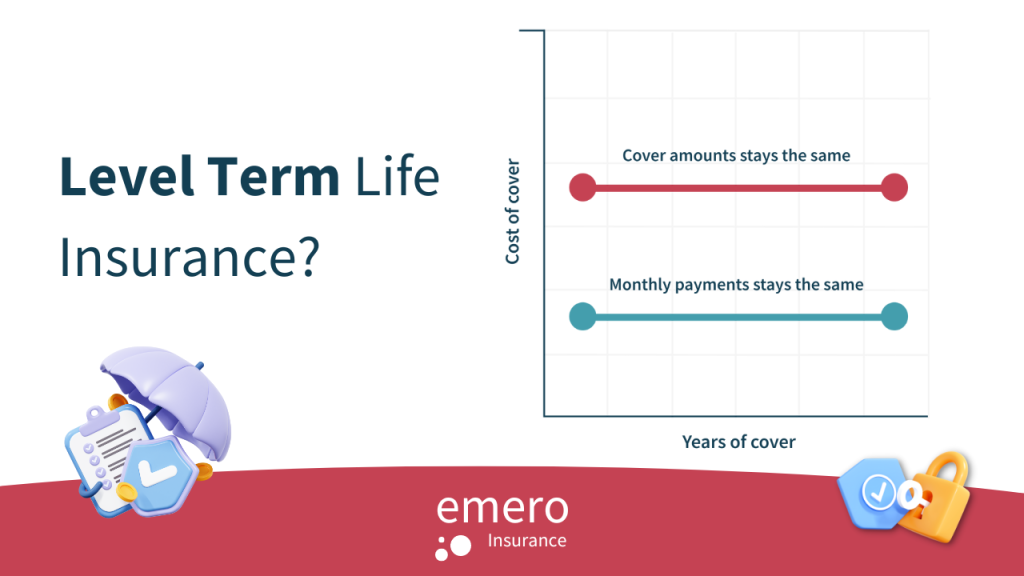

Level term life insurance policy is a plan that lasts a collection term normally between 10 and thirty years and includes a degree survivor benefit and degree costs that remain the exact same for the whole time the policy holds. This indicates you'll understand exactly just how much your payments are and when you'll need to make them, allowing you to budget plan appropriately.

Level term can be a great option if you're wanting to acquire life insurance coverage for the first time. According to LIMRA's 2023 Insurance Measure Research Study, 30% of all grownups in the United state requirement life insurance policy and do not have any kind of plan. Level term life is foreseeable and budget friendly, which makes it one of the most popular kinds of life insurance policy.

A 30-year-old male with a similar profile can expect to pay $29 per month for the very same protection. AgeGender$250,000 protection quantity$500,000 insurance coverage amount$1 million coverage amount20Female$15$23$34Male$19$29$4830Female$15$23$37Male$18$29$4940Female$22$35$61Male$25$43$7550Female$44$78$139Male$57$102$18860Female$108$194$355Male$149$268$500 Collapse table Technique: Ordinary regular monthly rates are calculated for male and women non-smokers in a Preferred health category obtaining a 20-year $250,000, $500,000, or $1,000,000 term life insurance coverage plan.

Rates may vary by insurer, term, coverage amount, health class, and state. Not all plans are readily available in all states. Price image valid since 09/01/2024. It's the cheapest kind of life insurance policy for most individuals. Degree term life is much a lot more economical than a comparable whole life insurance policy plan. It's simple to take care of.

It enables you to budget and strategy for the future. You can quickly factor your life insurance policy into your budget since the costs never ever alter. You can prepare for the future equally as quickly due to the fact that you know precisely just how much cash your loved ones will certainly receive in case of your absence.

What is Increasing Term Life Insurance? Key Facts

This is true for individuals who stopped cigarette smoking or that have a health problem that deals with. In these instances, you'll usually have to go with a brand-new application process to obtain a much better price. If you still require insurance coverage by the time your level term life plan nears the expiry day, you have a few choices.

The majority of degree term life insurance policy policies feature the option to restore coverage on an annual basis after the initial term ends. The expense of your plan will certainly be based upon your present age and it'll increase yearly. This might be a great option if you only need to prolong your coverage for one or two years otherwise, it can get pricey quite swiftly.

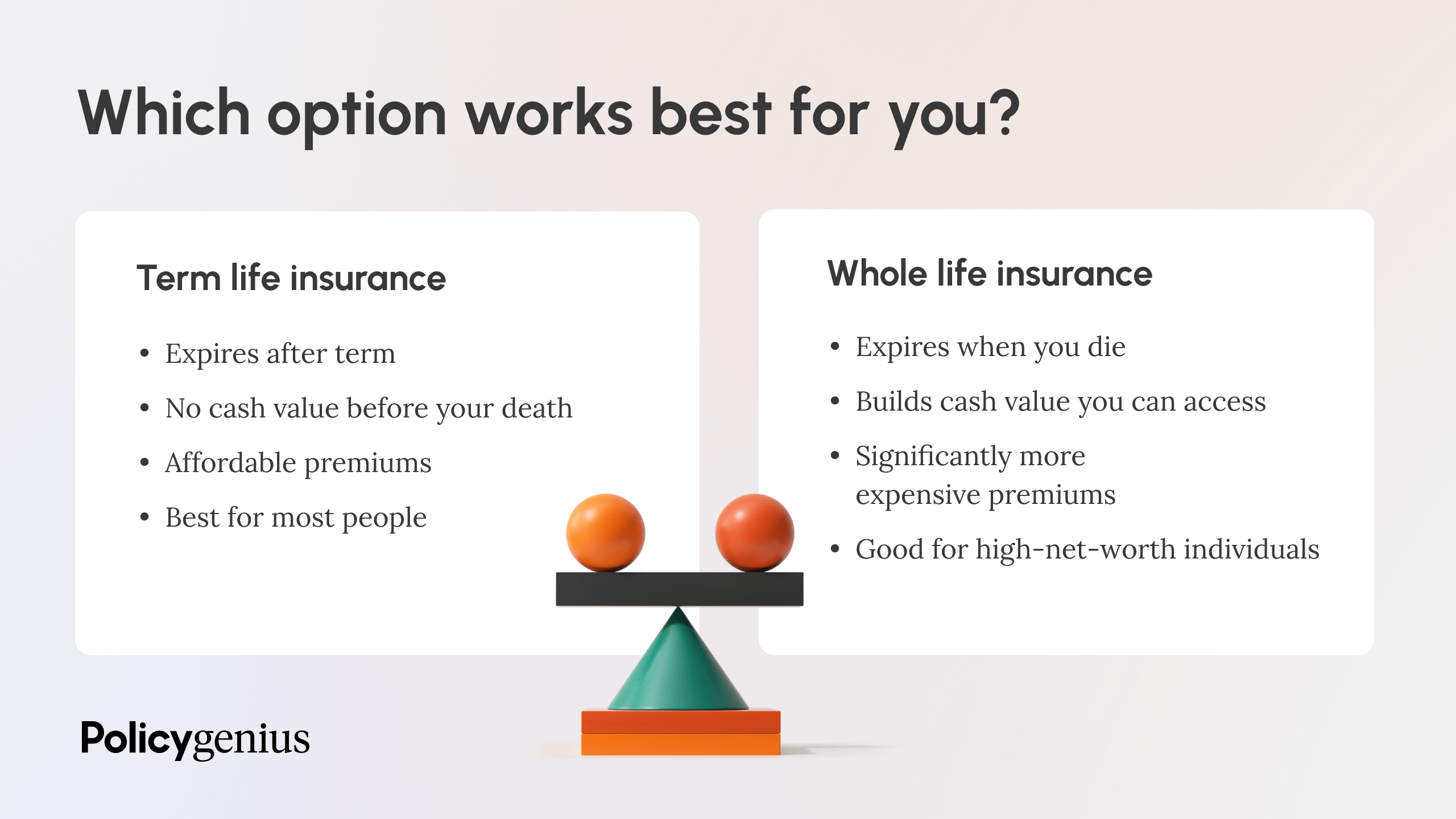

Degree term life insurance is one of the least expensive coverage options on the marketplace due to the fact that it uses fundamental security in the kind of fatality advantage and just lasts for a set time period. At the end of the term, it ends. Entire life insurance, on the various other hand, is considerably much more costly than level term life because it doesn't end and includes a money worth function.

Rates may differ by insurance company, term, protection quantity, wellness class, and state. Not all policies are available in all states. Price picture valid as of 10/01/2024. Degree term is a great life insurance policy alternative for the majority of people, but relying on your coverage needs and personal circumstance, it could not be the most effective fit for you.

Annual eco-friendly term life insurance coverage has a term of just one year and can be renewed yearly. Yearly eco-friendly term life costs are initially lower than level term life premiums, however rates increase each time you restore. This can be a great alternative if you, for instance, have simply stop cigarette smoking and require to wait 2 or 3 years to request a degree term policy and be qualified for a lower rate.

With a decreasing term life policy, your survivor benefit payment will reduce with time, yet your settlements will remain the same. Lowering term life policies like home mortgage security insurance policy generally pay out to your lender, so if you're seeking a policy that will certainly pay out to your enjoyed ones, this is not a great fit for you.

What is Term Life Insurance With Accidental Death Benefit? How It Works and Why It Matters?

Enhancing term life insurance policy plans can assist you hedge against rising cost of living or plan monetarily for future kids. On the various other hand, you'll pay even more ahead of time for much less insurance coverage with a boosting term life policy than with a degree term life plan. Increasing term life insurance. If you're unsure which kind of policy is best for you, dealing with an independent broker can help.

Once you have actually made a decision that level term is right for you, the following action is to purchase your policy. Here's just how to do it. Determine just how much life insurance policy you need Your coverage quantity must attend to your family members's long-term financial demands, including the loss of your income in the event of your death, in addition to financial obligations and everyday expenditures.

One of the most prominent type is now 20-year term. Most firms will certainly not market term insurance to an applicant for a term that ends previous his or her 80th birthday celebration. If a policy is "eco-friendly," that means it continues active for an extra term or terms, up to a specified age, also if the health of the guaranteed (or various other variables) would cause him or her to be denied if he or she obtained a new life insurance policy policy.

Costs for 5-year sustainable term can be level for 5 years, after that to a brand-new rate mirroring the brand-new age of the guaranteed, and so on every five years. Some longer term policies will certainly assure that the costs will not enhance during the term; others don't make that assurance, allowing the insurance coverage company to raise the rate during the plan's term.

What is Direct Term Life Insurance Meaning? Comprehensive Guide

This indicates that the policy's owner can change it into an irreversible kind of life insurance policy without extra proof of insurability. In many sorts of term insurance policy, consisting of property owners and vehicle insurance, if you have not had an insurance claim under the policy by the time it expires, you obtain no reimbursement of the premium.

Some term life insurance policy customers have been dissatisfied at this result, so some insurance providers have actually produced term life with a "return of premium" feature. The premiums for the insurance coverage with this feature are usually considerably greater than for policies without it, and they generally call for that you keep the policy in force to its term otherwise you surrender the return of costs advantage.

Degree term life insurance costs and fatality benefits remain regular throughout the policy term. Level term life insurance policy is typically much more inexpensive as it does not develop cash money worth.

While the names often are used mutually, degree term protection has some essential differences: the premium and fatality advantage stay the very same for the period of coverage. Level term is a life insurance policy policy where the life insurance coverage premium and survivor benefit continue to be the same throughout of protection.

{kind=link}

Table of Contents

Latest Posts

Best Funeral Plans For Over 50s

Burial Insurance

Funeral Insurance For Over 50s

More

Latest Posts

Best Funeral Plans For Over 50s

Burial Insurance

Funeral Insurance For Over 50s